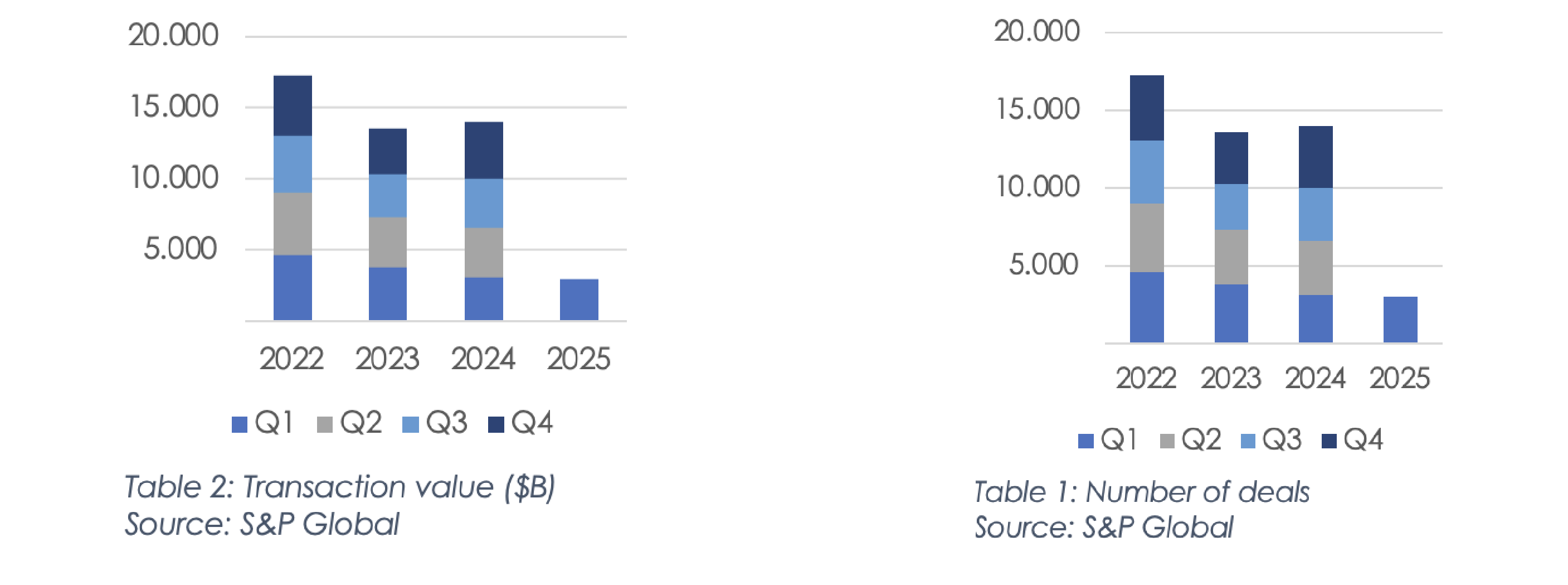

The mergers and acquisitions (M&A) landscape across Europe, in the first seven months of 2025 has been marked by complexity and contradiction. While both Western Europe and the Western Balkans are navigating a challenging macroeconomic situation, their respective M&A narratives reveal contrasting dynamics and strategic adaptation. Across Europe, a "flight to quality" has led to a notable rise in total deal values, even as overall deal volumes have remained low or declined in some regions. In Q1 2025, Europe's total deal volume saw a minor decrease of 5% compared to Q1 2024, dropping from 3,141 to 2,981 deals. Despite this reduction in volume, transaction values across Europe saw a modest year-over-year increase of 3.6%. (S&P Global). Globally, deal volumes fell 9% in the first half of 2025 compared to 2024, while deal values increased 15% (PwC).

2025 began with cautious optimism, continuing atrend in which deal volumes declined but total deal values rose, signalling a shift toward larger, more strategic transactions. Deals valued over $1 billion rose by 19% year-on-year, and those exceeding $5 billion increased by 16%, reflecting a concentration of capital on high-quality assets. Across EMEA, overall deal volumes and values declined 6% and 7% respectively, largely due to fewer mega deals in the UK. However, financial services deals in Europe increased by 6% in volume and saw significant rises in deal values, while manufacturing and distribution grew by 2%, with Scandinavia and Germany seeing 6-10% growth, partly due to investments in aerospace and defence.

Mergers and acquisitions are increasingly adopted across companies of all sizes: while nearly all large, listed firms now have formal M&A strategies, a growing number of small and medium-size denterprises (SMEs) are also engaging in deals both as buyers and sellers. The rise of private equity firms is intensifying deal competition, while advances in technology provide dealmakers with better data and analytics, fuelling further growth. While private equity is on the rise, these funds face pressure to invest the large amount of money they’ve raised but haven’t used yet. A notable shift in focus from internal rate of return (IRR) to distributed to paid-in capital (DPI) is compelling these firms to generate cash by selling assets, creating a new wave of sell-side opportunities. Deal-making is evolving, with due diligence now including broader checks on ESG, AI risks, and cyber security. (PwC, Dealsuite article).

The macroeconomic picture in the Western Balkans is a mixed picture. The World Bank projected a modest economic growth slowdown for the region in 2025, forecasting a combined growth of 3.2%, a downward revision from earlier estimates. This was confirmed by a report from the European Commission, which noted a significant decrease’s real GDP growth to 2.3% in the first quarter of 2025.

The figures, however, reveal acritical difference. Serbia, the region’s largest economy, experienced a notable slowdown in GDP growth to 2.0% in Q1 2025. This was in contrast to countries like Albania, North Macedonia, and Kosovo, which managed to maintain growth rates above 3% during the same period. Similarly, net foreign direc tinvestment (FDI) in flows fell in most countries, particularly in North Macedonia and Serbia. This under scores the need for a targeted, country-specific approach to M&A.

The M&A landscape is also being shaped by long-term strategic drivers, notably the EU’s €6 billion Growth Plan, which channels investment into green and digital transitions. Additionally, “near-shoring”, where multinationals move operations closer to European markets to reduce supply chain risks, is influencing activity, though its adoption varies by country. Overall, these dynamics reflect a broader trend where Europe’s M&A market is becoming more selective, with leading acquirers using programmatic, data-driven strategies and rigorous due diligence to capture value in both mature and emerging markets. (World Bank, Dealsuite article).

A powerful force shaping the M&A market in the Western Balkans is the European Union’s new Growth Plan, backed by a €6 billion financial facility. This plan is designed to accelerate the region's convergence with the EU's single market by directing investments into critical areas such as energy, transport, and digital infrastructure. This policy framework serves as a strategic roadmap for investors, effectively de-risking deals that align with these EU priorities. (European Commission, Dealsuite article).

One of the most prominent trends is near-shoring, a strategy by multinational firms to relocate operations closer to end markets to mitigate geopolitical and logistical risks and to lower production costs. Data from the FIW Institute indicates that this trend is gaining traction in Bosnia and Herzegovina, Kosovo, and North Macedonia, where actual FDI inflows have consistently exceeded pre-pandemic trends. However, this trend has not been as evident in Albania and Serbia, where FDI inflows have fallen below simulated projections. (FIW)

A growing challenge that has also become a driver for M&A is the severe shortage of skilled labour. A conference in Montenegro noted that 40% of employers in the Western Balkans cannot recruit workers with the necessary skills. In response, a trend known as "acqui-hiring" - the acquisition of a company primarily to secure its skilled personnel, is gaining popularity (IOM, Dealsuite article).

The M&A transactions completed in the first half of 2025 illustrate these emerging trends. Deals in both Western Europe and the Western Balkans demonstrate a clear focus on consolidation, strategic positioning, and the acquisition of new capabilities.

In the EU, some of the most notable transactions were driven by consolidation and strategic positioning across various sectors. The food and beverage industry saw a significant transaction with the Danish brewing group Carlsberg acquiring the UK-based soft drinks producer Britvic for £3.3 billion, an example of consolidation in the sector. In the financial services sector, a major merger valued at $13.7 billion took place in Italy between Banca Monte dei Paschi and Mediobanca Banca di Credito Finanziario, underscoring the ongoing consolidation trends in Southern European banking. The private equity space was also active, with French firm Ardian acquiring a 60% stake in three prestigious Parisian real estate properties from Kering SA for $860 million. Expanding beyond traditional Western European hubs, BlackPeak Capital made a growth equity investment in Affinity Life Care, a Romanian network of senior care centers. This transaction marks a key entry of a private equity fund into the senior care sector in an EU country in Central and Eastern Europe (Schoenherr).

In the Western Balkans, deals showcased a combination of foreign industrial investment and public-sector-driven technological development. One of the most significant industrial M&A transactions in Southeast Europe this year involved a joint venture between Molins and TITAN acquiring an 80 per cent stake in Baupartner, a leading precast concrete and steel structures company in Bosnia and Herzegovina, to support its regional expansion. In Serbia, the Netherlands-based CEE-BIG B.V. gained full control of NEPI Real Estate Project One, a deal that received unconditional approval from the Serbian competition authority, highlighting sustained interest in the country’s real estate market.The Albanian government took a public-sector initiative to foster a knowledge-based economy by investing €8.8 million in the AI startup Machine Thinking Lab, founded by a former CTO of OpenAI. Additionally, the K4S6 fund made an equity investment in Patoko, Albania’s fastest-growing mobility and service-booking platform, reflecting the growing maturity of the nation’s startup ecosystem. (Schoenherr, Chambers and Partners, The Recursive).

The European M&A market isentering a phase of greater selectivity and maturity, marked by a sustained focus on strategic, high-value transactions and an expanded due diligence scopeto address ESG, technology, and geopolitical risks. In the Western Balkans, the transition from opportunistic to structured and programmatic dealmaking is being accelerated by EU policy support and the region’s economic convergence agenda.

In this evolving landscape, Systema Capital Partners sees a unique opening for investors who can combine disciplined execution with deep regional understanding. Operating at the intersection of Western European capital markets and local market realities, we are positioned to identify under-the-radar opportunities, structure them in alignment with EU priorities, and deliver sustainable value creation. Our approach, anchored in rigorous financial analysis, robust governance standards, and a trusted regional network, enables us to connect high-quality Western investors with credible local businesses ready for the next stage of growth.

Despite ongoing challenges, notably in transparency, institutional maturity, and the cost of capital, the Western Balkans offer a fertile environment for those prepared to take a long-term, partnership-driven approach. At Systema Capital Partners, we believe that by leveraging our international network, sector expertise, and data-driven methodologies, we can help our clients not only navigate these markets but also shape their future.

.svg)