Serbia is entering its next phase of M&A activity from a stronger macroeconomic position than it had just a few years ago. The country received its first-ever investment-grade sovereign rating from S&P in October 2024, a BBB– rating with a stable outlook that was reaffirmed in March 2026. Official National Bank reports show that Serbia recorded EUR 5.2 billion in FDI inflows in 2024, a record level, which fully covered the current account deficit for the tenth consecutive year. For dealmaking, this matters because a more stable macro and financing environment tends to support investor confidence, valuation visibility, and transaction execution.

Yet the next phase of M&A in Serbia and the broader SEE region is likely to be influenced not only by capital availability but also by demographic trends. In the transition economies of emerging Europe, many privately owned businesses were established in the early 1990s, at the beginning of the shift away from central planning.Those founders are now nearing retirement age, rendering succession an increasingly urgent — and still relatively new — challenge for the region.

In Serbia, this issue is especially significant because family businesses are both a relatively recent phenomenon historically and a critically important aspect of ownership. Formal succession planning systems remain underutilised, and the data confirms that ownership remains highly concentrated. In Central and Eastern Europe, 64% of family businesses are still run by the first generation, compared to 32% globally.1 In other words, a significant portion of the regional business landscape is still under the control of founders rather than subsequent generations.

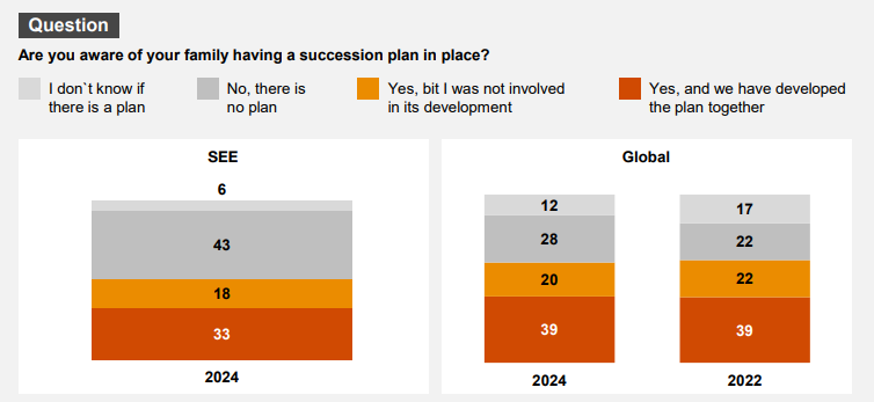

The scale of the challenge becomes even clearer in the succession data available for SEE. Evidence from the region shows that only about half of respondents say their family business has a succession plan, while 43% report that no such plan exists and another 6% do not know whether one exists at all. The same survey indicates that 53% consider the current generation’s ability or readiness to retire as a difficult aspect of succession.2 In Serbia and across the wider transition economies of Southeast Europe, this reluctance often has a deeper historical reason. Many founders built their companies during the institutional volatility of the 1990s, when entrepreneurship was not merely a route to profit but a means of creating stability, status, and family security in a newly emerging market economy. As a result, the business is often seen not just as a financial asset but as an extension of the founder’s identity and life’s work. This helps explain why succession can be emotionally challenging, even where the economic rationale for transition is clear. Framed this way, M&A should not be viewed only as a route to liquidation but also as a tool for legacy preservation: a way to ensure continuity, protect what has been built, and transfer leadership in a more structured manner. Put simply, many businesses in the region are entering a phase in which continuity of ownership and leadership can no longer be left to informal understanding or postponed indefinitely without risking serious business consequences.

This is the point where succession ceases to be merely a family issue and begins to become a matter of corporate finance. A generational transfer is never solely about passing shares; it also involves transferring control, decision-making power, relationships with management, accumulated expertise, and often the internal balance among family members. That is why corporate governance experts point to tools such as succession plans, family councils, and family protocols: continuity must be planned, not taken for granted.

The difficulty is that this design is often missing. Across the region, many founders still want to keep the business in family hands, yet the planning required to make that outcome realistic is often insufficient. The gap between intention and preparation, left unaddressed, eventually becomes an operational, strategic and financial problem — not simply a private family discussion. At that stage, external solutions become more relevant: not because the business is necessarily under stress, but because the ownership transition can no longer be managed internally.

In that context, M&A increasingly becomes part of the solution rather than merely an exit route. The choice is rarely a binary decision between keeping the company within the family and selling it outright. Founders may instead consider a broader range of options: a minority sale that reduces concentration risk while maintaining involvement, a strategic partnership that brings in capital and capabilities alongside family management, a majority sale with a phased transition, or a full exit when no internal successor is prepared or willing to take over. Regional private equity funds are becoming progressively more relevant in this spectrum because they can act, in effect, as institutional successors: not replacing the family’s legacy, but providing the governance, professionalisation, and bridge leadership that the next generation may not yet be ready to provide immediately. In that sense, succession is becoming an increasingly important source of deal flow because ownership transitions more frequently require structured transaction solutions.

This is especially relevant in sectors such as manufacturing and agriculture in Serbia, where ownership is often still tightly held, operational know-how remains highly dependent on founders, and the practical challenge of transferring control can be greater than the legal transfer of shares itself.

For a founder, awell-structured M&A deal does not necessarily equate to a final exit. Particularly in transactions involving financial investors, it can enable the seller to realise part of the value generated over time while maintaining exposure to future growth through a minority stake. This is the principle of rollover equity: taking cash at closing while remaining invested in the next phase of the business.

The key question, therefore, is not only whether to sell but also how to structure the transaction. In many cases, a deal can provide immediate liquidity, access to a stronger or more institutional partner, and continued involvement in future upside. This is even more important in today’s environment, where post-deal value creation relies less on automatic multiple expansion and more on execution, growth, and earnings quality. In this context, a generational transition does not necessarily mean an exit; when properly structured, it can signal a new phase for the company, supported by stronger governance, deeper capital, and a further cycle of value creation.

For founders, however, the transaction is only part of the story. Once all or part of the business is sold, the nature of personal wealth changes fundamentally. For years, a founder’s net worth has typically been concentrated in a single illiquid operational asset exposed to commercial, managerial, and industry risks. After a transaction, that value is converted into liquid capital that must be protected, allocated, and ultimately transferred. Recent family-business research increasingly frames long-term success in precisely these broader terms: not only as the succession of the business itself but as the meaningful transfer of capital across generations.

At that point, the conversation moves beyond the deal and into post-transaction planning. The questions are not limited to investment management in a narrow sense; they also include family governance, inheritance planning, diversification, capital preservation and the future role of the former owner. In the Serbian market, the growth of private-banking and advisory services confirms that this infrastructure is increasingly available in-country and is not only an offshore consideration.

From this perspective, generational transition involves more than just an ownership transfer; it also signifies a wider capital shift. That’s why succession-driven M&A is important not only as a means of ensuring business continuity but also as the moment when entrepreneurial value turns into family wealth that needs to be structured for the next generation.

At Systema Capital Partners, we collaborate with founders during this critical phase — from exploring whether and how a transaction is appropriate, through to deal structuring, choosing the right counterparty, and addressing governance issues that arise after completion. Serbia and the broader Western Balkans are entering their first notable cycle of succession-driven M&A. In a market where specialised advice in this area remains scarce, the guidance a founder receives at this stage can influence outcomes far beyond the transaction itself.

1 PwC,“2023 Family Business Survey, Central and Eastern Europe,” PwC CEE, 2023.Available at: cee.pwc.com/2023-family-business-survey-in-cee.html

2 PwC,“Global NextGen Survey 2024 – SEE Report,” PwC Serbia, 2024. Available at:pwc.rs/en/publications/nextgen-survey.html

.svg)